The Complete Guide to Insurance Analytics

From Descriptive to Predictive Insights: Data, Decisions, and Growth

Inhalt

- 1. Executive Summary

- 2. Fundamentals

- 3. Data Foundations

- 4. Benefits & Business Value

- 5. Types of Analytics

- 6. Roles & Responsibilities

- 7. The Analytics Process

- 8. Challenges & Opportunities

- 9. KPIs

- 10. Governance & Compliance

- 11. Best Practices

- 12. Operating Models

- 13. Workforce

- 14. The Future

- 15. Guidewire Solutions

- 16. Conclusion

Insurance Analytics: From Data to Decisions

Insurance analytics has become a foundational capability for today's property and casualty insurers as risk complexity, regulatory expectations, and competitive pressures continue to increase. If Intelligent Insurance is applying the right information at the right time to inform better actions, insurance analytics is the critical process of transforming raw data into actionable insights, information that can drive better decisions.

Insurance analytics is the systematic application of data, statistical methods, and predictive models to support decision-making across pricing, underwriting, claims management, and fraud detection. In P&C insurance, analytics enables carriers to translate data into insight and insight into action within core operational workflows. And in the world of AI, the structures and disciplines required for effective insurance analytics provide a foundation for insurers to evaluate and implement new capabilities from AI systems into their operations.

Modern insurance analytics spans descriptive, diagnostic, predictive, and prescriptive techniques. Together, these approaches allow insurers to move from raw data to informed decisions by identifying performance drivers, forecasting future outcomes, and recommending optimal actions that correspond with corporate goals. Increasingly, these capabilities are delivered through machine learning and AI-driven models that connect data directly to prediction and decision logic. These decisions may become automated based on model output, or they could remain human choices, aided by information the models provide. When analytics is embedded at the point of decision, it reduces loss volatility, improves underwriting precision, and increases operational efficiency.

Industry analysts consistently report that insurers who operationalize analytics at scale outperform peers on profitability and loss-related metrics. By systematically linking data availability, analytics, and execution, predictive and prescriptive analytics enable a shift from reactive analysis to proactive, real-time decision support—driving measurable loss reduction and sustainable premium growth for P&C carriers.

This document provides a comprehensive overview of insurance analytics. It covers foundational concepts, analytics types, business value, governance and compliance considerations, implementation challenges, operating models, and emerging technologies shaping data-driven insurance operations across the P&C value chain.

Inhalt

- 00Executive Summary: Insurance Analytics in 90 SecondsJump →

- 01Fundamentals: What Is Insurance Analytics?Jump →

- 02Data Foundations: Building the Analytics-Ready Insurance Data LayerJump →

- 03Benefits and Business Value: Why Insurance Analytics MattersJump →

- 04Types of Insurance Analytics: Descriptive, Diagnostic, Predictive, and PrescriptiveJump →

- 05Roles and Responsibilities in Insurance AnalyticsJump →

- 06In Motion: The Analytics Process in InsuranceJump →

- 07Finding Direction: Challenges and Opportunities in Insurance Data AnalyticsJump →

- 08Measuring What Matters: KPIs for Insurance Analytics PerformanceJump →

- 09Staying Aligned: Governance and Compliance in Insurance DataJump →

- 10Shaping Excellence: Best Practices for Analytics in InsuranceJump →

- 11Operating Models: Building and Scaling Insurance Analytics TeamsJump →

- 12Empowering the Workforce: Data Literacy and Change ManagementJump →

- 13Looking Ahead: The Future of Predictive and Prescriptive AnalyticsJump →

- 14From Insight to Action: Guidewire Analytics SolutionsJump →

- 15Conclusion: Insurance Analytics as a Strategic AdvantageJump →

Executive Summary: Insurance Analytics in 90 Seconds

Insurance analytics is the systematic use of data, statistical methods, and predictive models to support decision-making across pricing, underwriting, claims, fraud detection, and customer management. In property and casualty insurance (also known as general insurance), analytics connects data to action by transforming raw data into useful information. This includes translating risk signals into decisions that shape profitability and loss outcomes, as well as analyzing operational data to optimize decisions across an insurer's functions.

Analytics directly influences the financial performance of P&C insurers. Pricing accuracy, loss ratio control, claim severity management, fraud detection, and customer retention all depend on the insurer's ability to anticipate outcomes and act consistently at scale. Insurers with mature analytics capabilities routinely outperform peers on combined ratio, expense ratio, and growth metrics by reducing uncertainty and improving decision quality.

As risk complexity increases, traditional reporting and retrospective analysis are no longer sufficient. But many insurers struggle to operationalize analytics despite significant investment. Common obstacles include fragmented data environments, inconsistent data quality, inefficient modeling processes, limited real-time access to insights, growing regulatory scrutiny of model-driven decisions, and shortages of analytics talent with insurance domain expertise.

Rather than only analyzing results after the fact, leading P&C insurers are embedding analytics directly into core workflows using predictive and prescriptive models supported by machine learning and AI. Analytics is increasingly used to guide underwriting decisions, route claims, detect fraud earlier, and personalize customer interactions in real time. The objective is not analytics maturity for its own sake, but measurable improvement in loss performance, efficiency, and competitive differentiation.

This guide provides a comprehensive overview of insurance analytics, including foundational concepts, data prerequisites, analytics types, organizational roles, lifecycle processes, governance and compliance considerations, performance measurement, operating models, workforce enablement, emerging trends, and the technologies that support analytics-driven insurance operations. It does not cover the analytics involved in determining appropriate reserve levels for insurers, nor does it cover the specific analytics that can be used in investing and asset management. However, many of the ideas and principles will be relevant in these areas as well.

Insurance executives, analytics and data leaders, underwriting and claims operations managers, actuarial teams, technology decision-makers, compliance professionals, and anyone responsible for improving profitability, loss outcomes, or decision consistency in P&C insurance.

A Note About AI

Insurance analytics has always involved artificial intelligence (AI) in the broadest sense of the term: computer algorithms learning from experience (data). Any predictive model with optimized coefficients counts as AI. However, this guide acknowledges that when AI is now used in common language, large language models (LLMs) and generative AI (genAI) is what is meant. When the term "AI" is used in this guide we will be referring to LLMs, genAI and associated technologies (e.g. agents or multi-modal models).

A complete discussion on how to effectively implement AI-based systems is beyond the scope of this guide. For our purposes, AI is considered a tool that will impact how insurance analytics is conducted and implemented.

The impact that modern AI will have on insurance analytics is widespread, but the most likely one is changing the way humans interact with information. LLMs bring an understanding of the human language such that instructions and requests can be given in the form of expressions of intent, what is wanted, rather than in detailed spec documents or lines of code. This allows AI to summarize data and bring it to the fore, which has significant implications for insurance workflows and automation.

However, LLMs and genAI are inherently probabilistic in their output, with no guarantees of the repeatability required for many insurance applications. Their applicability to making the specific predictions typical of traditional statistical and machine learning techniques is questionable. We assume the continued relevance of these techniques. AI may change how actuaries and data scientists go about making predictive models, but it doesn't change the need to create these models and deploy them effectively into insurance workflows.

"AI succeeds when it solves real business problems."

Laura Drabik · Chief Evangelist, Guidewire

In this guide we focus on insurance analytics as a key component of Intelligent Insurance, defined as surfacing the right information at the right time in order to improve decisions. AI will change the workflows of adjusters, underwriters and others, and it may change how the provided information is accessed, but it will not change the need for accurate information at the right time that will improve insurance decisions.

How This Guide Is Structured

This guide is organized around the core lenses through which insurance analytics is designed, deployed, and evaluated. Each major section examines analytics from a specific operational perspective, such as data foundations, analytics methods, decision processes by insurance function (pricing, underwriting, etc.), organizational roles, governance controls, performance measurement, workforce enablement, and technology integration.

Key terms are defined within the context of the section in which they appear. A concept may therefore be explained differently across sections, reflecting its distinct role in analytics execution, governance, performance management, or organizational design. These definitions are intentionally contextual rather than abstract.

Throughout the guide, definitions and explanations emphasize:

- when a concept becomes relevant,

- how it operates within insurance workflows, and

- what outcomes it produces for insurers, customers, and regulators.

Insurance analytics is a system of interconnected data, models, decisions, and controls—not a collection of isolated techniques. The organization of this guide reflects that reality and is designed to support consistent reasoning across operational, strategic, and technical considerations.

Fundamentals: What Is Insurance Analytics?

Insurance analytics is the discipline that connects insurance data to decision-making across the property and casualty value chain. It encompasses the systematic use of statistical analysis, predictive modeling, and decision logic to inform pricing, underwriting, claims management, fraud detection, and customer engagement. In P&C insurance, analytics provides the mechanism by which raw data is transformed into consistent, repeatable, and auditable business decisions.

At its core, insurance analytics answers four fundamental questions that guide both operational execution and strategic planning:

- What happened? (Descriptive analytics)

- Why did it happen? (Diagnostic analytics)

- What is likely to happen next? (Predictive analytics)

- What is the best course of action? (Prescriptive analytics)

These analytics types function as a continuum rather than isolated capabilities. Descriptive reporting establishes baselines and operational visibility. Diagnostic analysis provides context by explaining drivers and correlations. Predictive models quantify future outcomes and opportunities. Prescriptive analytics operationalizes insight by guiding actions such as pricing adjustments, claim routing, or fraud investigation. And in circular fashion, descriptive analytics monitors the impact of changed (improved!) business processes. When combined, these capabilities reduce uncertainty and variability across insurance operations.

Modern insurance analytics operates on integrated data environments that draw from core policy, billing, and claims systems, supplemented by external data sources such as property intelligence, geospatial risk indicators, and behavioral signals. Governance controls ensure data quality and consistency before analytics outputs are delivered through dashboards, decision engines, or embedded workflows. This integration allows insights from analytics to be delivered at the right time, and to function as an active component of daily operations rather than a retrospective reporting function.

Too many make the mistake of focusing on technical challenges rather than the strategic questions of where to apply analytics as the solution to their business problems.

Chris Cooksey · Senior Director of Advanced Analytics, Guidewire

As outcomes are observed, analytics systems incorporate feedback to refine future decisions. Machine learning techniques enable models to be recalibrated as new data becomes available, improving accuracy over time. This creates a circular analytics capability in which decisions are informed by prior results, reinforcing performance improvement across underwriting, claims, and customer management.

Insurance analytics delivers the greatest value when it informs human and automated decisions. This requires that it be embedded directly into core operational systems. Rather than existing as standalone tools, analytical insights are integrated into insurance pricing, underwriting workbenches, claims workflows, and customer service platforms. This embedded approach supports automation where appropriate, as well as auditability and scale—ensuring that analytics-driven decisions are applied consistently at the point of execution, and in a way that builds trust.

Top Terms in Insurance Analytics Fundamentals

What is it? The systematic use of data, statistical methods, and models to generate insights and information that support insurance decisions. When is it relevant? Across the insurance lifecycle, from marketing, sales and distribution, to underwriting and pricing, and through to claims management, portfolio management, and customer renewals. What does it do? Transforms data into information, insights and recommendations. What outcome does it create? More accurate, consistent, and profitable insurance decisions. Examples Using expected loss models to inform insurance pricing, or claims models to guide efficient claims handling. What is it? Analysis that summarizes historical and current insurance data. When is it relevant? During operational monitoring, reporting, and governance activities. What does it do? Establishes visibility into performance metrics and trends. What outcome does it create? A factual baseline for accountability and oversight, and a shared understanding of what has occurred. Examples Dashboards tracking claim frequency and loss ratio trends. What is it? Analysis that explains why outcomes occurred. When is it relevant? When performance deviates from expectations. What does it do? Identifies drivers, correlations, and root causes. What outcome does it create? Insight into performance variability. Examples Analyzing loss ratio deterioration by geography. What is it? Statistical and machine learning techniques that use patterns in the data to forecast likely future outcomes. When is it relevant? Before decisions are made, especially when foreknowledge of the outcome would affect the decision made. What does it do? Estimates probabilities and expected values of future events. It informs a decision-maker of what is more or less likely to happen. What outcome does it create? Reduced uncertainty and improved anticipation of risk and opportunity. Examples Predicting claim severity at first notice of loss. What is it? Analytics that recommends or automates actions based on predictions. When is it relevant? At the point of decision execution within insurance workflows. What does it do? Guides or automates optimal actions, reflecting corporate direction based on the predicted information. What outcome does it create? Improved decision execution and measurable performance gains. Examples Routing claims to fast-track or special investigation. What is it? A mathematical or statistical representation of the patterns found in data. When is it relevant? Whenever analytics is embedded into workflows or otherwise operationalized. What does it do? Translates known data inputs into output predictions or scores. What outcome does it create? Quantified insight into risk or performance. Examples A loss frequency model that takes years in business, location, and square footage (i.e. known data) as inputs, and provides an expected change of having a claim. What is it? Analytics that is integrated directly into operational systems. When is it relevant? During real-time underwriting, claims, or service workflows. What does it do? Delivers insights at the point of action. What outcome does it create? Faster and more consistent execution. Examples Severity scores displayed in claim intake screens. What is it? The use of analytics to automatically execute decisions. When is it relevant? For high-volume, low-complexity decisions. What does it do? Reduces manual intervention. What outcome does it create? Lower cost and faster cycle times. Examples Automatic claim assignment based on risk score. What is it? The output of a predictive model providing an estimate of the likelihood and impact of future loss events. When is it relevant? During pricing, underwriting, and claims triage. What does it do? Quantifies uncertainty, through the use of probabilities and expectations. What outcome does it create? Better alignment between risk and premium, risk and underwriting decisions, or claim severity and claim handling. Examples Predicting hail loss probability for property risks. What is it? An application of predictive analytics designed to identify suspicious or anomalous behavior. When is it relevant? During claims submission and review. What does it do? Flags high-risk transactions for referral or investigation. What outcome does it create? Reduced leakage and improved loss control. Examples Network analysis identifying collusive claim patterns.

Data Foundations: Building the Analytics-Ready Insurance Data Layer

Insurance analytics depends on the availability, quality, and structure of data long before models are built or insights are delivered. Having solid foundations for how an insurer handles, collects, stores and accesses data is critical, and forms connective tissue between operational systems and analytical decision-making. Operational systems generate the data that analytics needs access to in order to generate insights. Without a reliable data layer, analytics initiatives struggle to produce consistent, trustworthy outcomes, regardless of model sophistication.

An analytics-ready insurance data layer integrates core internal data sources, including policy, billing, claims, and customer information, with relevant external data such as property characteristics, geospatial risk indicators, weather history, and socioeconomic signals. This data must be standardized, governed, and continuously validated to ensure it reflects real-world exposure and operational reality. Fragmented systems, inconsistent definitions, and incomplete records introduce friction that limits the effectiveness of downstream analytics.

The data layer must facilitate two separate use cases for insurance analytics. One is to store historical transactions so that this data can be used for analysis and model-building. Data structures for efficient daily processing are different from those used for efficient storage, and both of these are different from how data is structured for analytics. An analytics-ready data layer facilitates these structural transitions to make data easily accessible for analytics projects.

Another use case is to provide data as inputs to operationalized predictive models in real-time workflow environments, in order for those models to provide predictions. Data structures for this application are the same as those for daily processing, except that the predictive models may require additional fields and data transformations.

| Historical / Analytics Storage | Real-Time Operational Inputs | |

|---|---|---|

| Purpose | Store historical transactions for analysis and model-building. | Provide data as inputs to operationalized predictive models so they can generate predictions. |

| Data structure | Structured for efficient analytics access — distinct from both daily-processing and storage formats. | Same structure as daily processing, with additional fields and transformations the models require. |

| Operating context | Analysis and model-building projects. | Real-time workflow environments. |

Modern insurers must design data foundations and use tools that support both the creation of and real-time use of analytical models. A well-architected data layer balances these needs, ensuring data is accessible at the speed required by the decision it supports.

Data quality in both use cases directly influences the accuracy of predictive and prescriptive analytics. Missing attributes, delayed ingestion, or poorly aligned data definitions can distort or limit loss forecasts, pricing signals, and claim severity estimates. Equally important is data representativeness. If certain geographies, risk types, or customer segments are underrepresented or inconsistently captured, analytics outputs may reinforce blind spots rather than reveal insight.

"The first component is data. Data is at the center of the challenge and the opportunities set before insurers..."

Chris Cooksey · Senior Director of Advanced Analytics, Guidewire

Data bias is a foundational challenge in insurance analytics. Bias can emerge when historical data reflects legacy underwriting practices, uneven claims handling, or structural gaps in data collection. Left unaddressed, these biases propagate through analytics pipelines, leading to skewed risk assessments, suboptimal pricing decisions, and unintended disparities in outcomes. Addressing data bias at the foundation stage through identification, mitigation, and continuous monitoring is essential to producing analytics that support both business performance and responsible decision-making.

Ultimately, strong data foundations enable a clear causal chain: reliable historical data feeds analytics; analytics using operational data informs decisions; decisions drive outcomes. When insurers invest in analytics-ready data foundations, they reduce uncertainty, improve loss predictability, and create the conditions for sustained profitability and disciplined growth.

Top Data Foundation Terms in Insurance Analytics

What is it? The structured collection of facts and statistics for reference or analysis. It includes records of all transactions for the insurer. When is it relevant? Before analytics models are developed or insights are embedded into operational workflows. What does it do? Provides a record of all transactions for the insurer. Provides information about risks insured and the environment in which the insurer operates. What outcome does it create? If organized and made accessible, reliable information for analytics. Examples Policy, claims, and billing data, or information about the insured risks. What is it? The comprehensive understanding of an insurer's data. It is a model for how to understand the insurer's data. When is it relevant? When developing the strategy for how to organize and handle data. What does it do? Defines what data means and how it is structured for different purposes. What outcome does it create? A unified understanding of what data means, how it is structured and organized, and how it might be used. Examples Data definitions, maps of data flows, descriptions of data organization. What is it? Part of the insurer's system architecture that organizes data storage and flow. When is it relevant? When storing data and accessing it for daily operations, external reporting, and analytics. What does it do? Captures and organizes the insurance data that inform analytics. What outcome does it create? A coherent understanding of the role of data within the insurer's system architecture. Examples Data lakes or warehouses, data definitions, data model. What is it? Specific repositories of data that may be accessed for analytics. When is it relevant? When determining the data to support an analytics project. Data may need to come from different sources and be combined. What does it do? Stores and organizes data making it available for specific purposes. What outcome does it create? Accessibility to different types of data. Examples Policy tables, claim tables, external data repositories. What is it? The organization and format of data. When is it relevant? During data flows and data storage. What does it do? Defines how the data is organized, what each datum means and how it relates to other data. What outcome does it create? Clear understanding of what data means, what it can be used for, and how it might be transformed for other purposes. Examples Relational databases, flat files, normalized and de-normalized data. What is it? Data generated by an insurer's core operational systems. When is it relevant? During underwriting, claims handling, billing, and customer servicing, and during insurance analytics. What does it do? Captures exposure, transactions, and outcomes that inform analytics. What outcome does it create? Visibility into performance, risk selection, and loss drivers. Examples Claim severity histories, policy attributes, payment timelines. What is it? Third-party data sources used to enrich internal insurance data. When is it relevant? At underwriting, pricing, fraud detection, and risk assessment stages, and during insurance analytics. What does it do? Adds contextual signals that are not available from internal systems alone. What outcome does it create? More accurate risk differentiation and better insurance decisions. Examples Property hazard data, weather history, telematics signals. What is it? Data that supports the daily operations of an insurance company. When is it relevant? During sales, underwriting, pricing, claims adjusting, customer service, and any other daily function of an insurance company. What does it do? Makes available the information needed to run an insurance company. What outcome does it create? Efficient processes and smooth customer experiences. Examples Insured/prospect address, policy number, loss date. What is it? Data from previous insurance transactions. When is it relevant? During insurance analytics, which requires significant volumes of data. What does it do? Makes available collections of previous insurance transactions. What outcome does it create? Insurance analytics. Examples Data lakes or warehouses, relational databases, normalized data. What is it? Data that has been cleansed, structured, and governed for analytical use. When is it relevant? Data preparation for insurance analytics. What does it do? Makes available data for analytical tools and algorithms. What outcome does it create? Faster deployment of analytics use cases. Examples Flat files, de-normalized data, curated datasets. What is it? The accuracy, completeness, and consistency of insurance data. When is it relevant? Continuously, across ingestion, analysis, and reporting. What does it do? Ensures analytics outputs reflect real-world conditions. What outcome does it create? Improved trust in analytics-driven decisions. Examples Validated claim amounts, standardized coverage codes. What is it? The process of aligning data definitions and formats across systems. When is it relevant? When integrating data from multiple core platforms or vendors. What does it do? Enables consistent analytics and reporting. What outcome does it create? Reduced ambiguity and faster insight generation. Examples Harmonized loss cause codes across claim systems. What is it? Systematic distortion in data caused by historical, structural, or collection-related factors. When is it relevant? During data preparation and analytics model development. What does it do? Skews analytics outputs if left unaddressed. What outcome does it create? Inaccurate risk assessments and inconsistent outcomes. Examples Underrepresentation of certain regions or customer segments in historical data.

Benefits and Business Value: Why Insurance Analytics Matters

The business of insurance is not to create data or to facilitate analytics. If insurance analytics does not meaningfully improve business outcomes, it is simply an unjustified expense.

Insurance analytics creates business value by improving the quality, speed, and consistency of decisions across the property and casualty insurance value chain. In P&C insurance, profitability, loss performance, and customer outcomes are shaped by thousands of daily decisions—from pricing and risk selection to claims triage and settlement. Analytics enables insurers to operationalize insight at these decision points, transforming data into measurable financial and operational improvement.

When analytics is embedded across these decision points and reinforced through continuous feedback, insurers move toward intelligent insurance operations—where insight is systematically translated into action across underwriting, claims, and customer engagement.

At an operational level, analytics is costly and does not create value directly. Value is realized when analytics improves how decisions are made and executed. By reducing uncertainty, standardizing judgment, and enabling proactive action, insurance analytics strengthens underwriting discipline, controls loss costs, and improves operational efficiency. This decision-centric impact is what differentiates analytics leaders not only from peers that rely primarily on retrospective reporting or manual judgment, but also from those who invest in analytics without realizing value.

Industry research consistently shows a strong correlation between advanced analytics adoption and superior financial performance in P&C insurance. According to analysis by McKinsey & Company, insurers that embed advanced data and analytics into underwriting and operational processes can achieve loss ratio improvements of three to five points, new business premium growth of 10–15 percent, and retention gains of 5–10 percent in profitable segments. These gains are driven by more accurate risk selection, earlier intervention, and tighter execution—not by analytics in isolation.

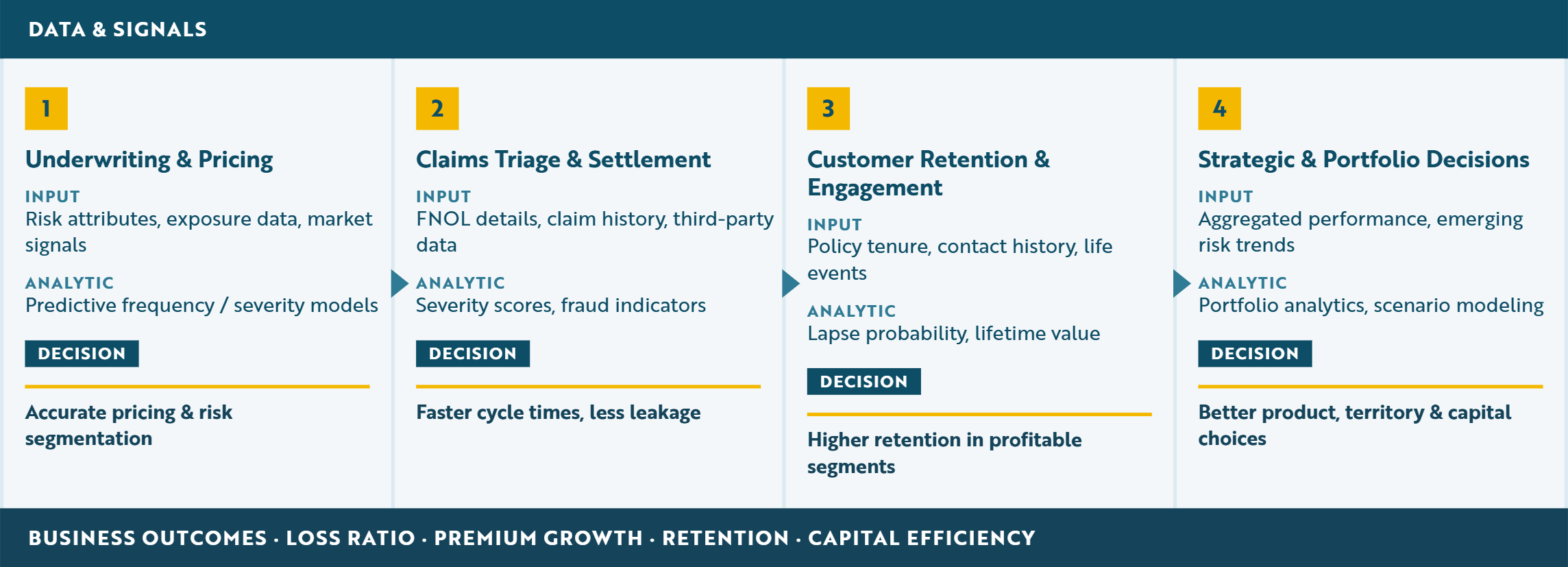

Insurers apply analytics at several high-impact decision points, each of which are discussed in more detail in following chapters:

- Underwriting and Pricing Decisions. Predictive models estimate expected loss frequency and severity, enabling more accurate pricing and risk segmentation. Analytics supports consistent application of underwriting guidelines and improves alignment between premium and exposure.

- Claims Triage and Settlement Decisions. Severity scores, fraud indicators, and workflow analytics guide claim routing, settlement strategy, and resource allocation. This improves cycle time, reduces leakage, and supports fair, timely outcomes.

- Customer Retention and Engagement Decisions. Predictive analytics can inform marketing decisions, as well as estimate lapse probability and customer lifetime value for existing customers. This enables proactive outreach and personalized renewal strategies that improve retention in profitable segments. Analytics can provide information about agent effectiveness and performance to improve distribution.

- Strategic and Portfolio-Level Decisions. Aggregated analytics informs product design, territory expansion, reinsurance strategy, and capital allocation by revealing emerging risk trends and performance patterns.

The cumulative effect of these improvements is both tactical and structural. Analytics-driven insurers reduce loss volatility, improve expense discipline, and adapt more effectively to changing risk environments. Over time, this compounds into sustained competitive advantage through more predictable profitability and faster response to market shifts.

"The predictive model is just one piece of a holistic effort to solve a problem. Centering on the business problem, not just the model, is the right approach."

Chris Cooksey · Senior Director of Advanced Analytics, Guidewire

Analytics produces information, but Intelligent Insurance runs on decisions. Insurance analytics delivers the greatest business value when embedded directly into core systems where decisions are executed. When analytics is integrated into underwriting, claims, and customer service workflows, insights are applied consistently and in real time—reducing delays, limiting manual overrides, and improving auditability. This embedded execution model is what allows analytics to scale from isolated use cases to enterprise-wide performance improvement.

Top Terms to Know in Benefits of Insurance Analytics

What is it? The measurable operational and financial metrics for the insurer. When is it relevant? In measuring the effectiveness of insurance operations. What does it do? Measures the financial health and operational efficiency of the insurer. What outcome does it create? Information on the financial health and operational efficiency of the insurer. Examples Combined ratio, new business close rates, average time to close a claim. What is it? The process of determining and implementing the price charged for insurance. When is it relevant? At quote, bind, and renewal for implementation, during insurance analytics in the creation/modification of the rating plan. What does it do? Ensures that the prices are not inadequate, not excessive, and not unfairly discriminatory. What outcome does it create? Competitive pricing that generates enough income to ensure financial stability. Examples Rating plan creation, rate deployment. What is it? The process of determining which risk to underwrite insurance for. When is it relevant? At quote, bind, renewal, and portfolio review stages. What does it do? Identifies the target customers the insurer wants to write. What outcome does it create? Written books of business that reflect corporate goals for the market to write. Examples Commercial underwriting, personal lines underwriting rules. What is it? Discrimination between insureds that represent different risks of loss. When is it relevant? During insurance pricing and risk selection. What does it do? Identifies which customers should be charged higher or lower premium. What outcome does it create? Prices that reflect risk without cross-subsidization. Examples Personal lines rating plans, commercial rates reflecting different risks. What is it? Efficient and effective execution of the insurer's underwriting strategy. When is it relevant? At quote, bind, renewal, and portfolio review stages. What does it do? Ensures that risks are selected, priced and underwritten according to corporate goals. What outcome does it create? Sustainable market presence and profitable performance. Examples Underwriting rules and processes, reviews of underwriter performance. What is it? The use of analytics to improve claims handling efficiency and outcomes. When is it relevant? From first notice of loss through settlement. What does it do? Guides triage, investigation, and settlement decisions. What outcome does it create? Reduced cycle time, lower leakage, and improved customer satisfaction. Examples Routing high-severity claims to senior adjusters using predictive scores. What is it? Paying more for a claim than an insurer is obligated to pay. When is it relevant? From first notice of loss through settlement. What does it do? Increases loss costs and reduces profitability. What outcome does it create? Results in the insurer making claim payments they should not be making. Examples Unidentified fraud, poor claim adjusting. What is it? Claims paid plus adjustment expenses divided by earned exposures. It is also defined as the claim frequency multiplied by the claim severity. When is it relevant? In performance measurement and insurance pricing. What does it do? Indicates the cost of insured losses per exposure. Does not measure expenses not allocated to the specific claim. A loss cost of $1000 indicates that the average claim payment for every unit of exposure is $1000. What outcome does it create? Visibility into insurance pricing and loss control effectiveness. Examples Analyzing loss costs to determine insurance prices, tracking loss costs for claim department performance. What is it? The ability to deliver insurance services with minimal cost and delay. When is it relevant? Across underwriting, claims, billing, and service operations. What does it do? Reduces friction and manual effort in insurance processes. What outcome does it create? Lower expense ratios and faster service delivery. Examples Automating low-complexity claims using analytics-driven rules. What is it? The chance that a current customer will not renew their policy. When is it relevant? Customer service, portfolio management, insurance pricing. What does it do? Reflects customer satisfaction with prices and service, as well as brand loyalty. What outcome does it create? Visibility into how an insurer's book of business evolves. Examples Analytics models predicting lapse probability.

Types of Insurance Analytics: Descriptive, Diagnostic, Predictive, and Prescriptive Analytics

Insurance analytics is best understood as a decision loop, not a collection of standalone techniques. The process is not strictly linear or circular, but generally moves forward by cyclically using different types of analytics to surface information to improve decisions. Insurance analytics is thought of as a closed loop when new actions based on analytics are monitored and reviewed so as to refine the next round of analytics.

Descriptive, diagnostic, predictive, and prescriptive analytics work together to transform data into decisions and decisions into outcomes across the property and casualty insurance lifecycle. Each analytics type answers a distinct question, and value is realized when all four operate to reinforce one another.

Framed as a decision loop, the four types of insurance analytics function as follows:

| Analytics type | Question it answers | What it does |

|---|---|---|

| Descriptive analytics | What happened? | Establishes visibility into historical performance and current state. |

| Diagnostic analytics | Why did it happen? | Explains drivers, correlations, and root causes behind observed outcomes. |

| Predictive analytics | What is likely to happen next? | Estimates future risk, behavior, or performance before decisions are made. |

| Prescriptive analytics | What is the best course of action? | Recommends or executes actions that optimize business outcomes. |

Predictive analytics is not “one and done.” Outcomes generated by prescriptive decisions feed back into descriptive measurement, enabling ongoing refinement and control.

Descriptive Analytics: Establishing Operational Visibility

Descriptive analytics summarizes historical and current data to provide a factual baseline for decision-making. In P&C insurance, this includes metrics such as claim frequency, loss ratio trends, quote conversion rates, expense ratios, and customer engagement levels. Descriptive insights support operational monitoring, regulatory reporting, and performance benchmarking by answering what has occurred and where performance stands today.

To draw an analogy to rafting down a river, descriptive analytics is looking around at the surface of the water. It tells you where you are, how close to the banks of the river, how fast the water is moving and if it is accelerating, etc.

Typical outputs include dashboards, standard reports, and visualizations that track key performance indicators across underwriting, claims, billing, and service operations. While descriptive analytics does not drive decisions directly, it is essential for perspective on the current state of operations and the effectiveness or impact of prior actions taken. It plays a valuable role in evaluation, as well as transparency, accountability, and governance.

Diagnostic Analytics: Explaining Performance Drivers

Diagnostic analytics builds on descriptive insight by attempting to explain why outcomes occurred. It identifies contributing factors, relationships, and patterns that influence performance. In insurance operations, diagnostic analytics is used to analyze loss ratio deterioration, identify claim severity drivers, understand pricing variance, or explain differences in performance across regions, products, or customer segments.

In the rafting analogy, diagnostic analytics looks under the water to identify the shape of the riverbed that guides the flow of water, as well as the placement of rocks and other obstacles that disrupt that flow.

This layer relies on techniques such as segmentation, correlation analysis, drill-down exploration, and comparative analysis. Diagnostic analytics supports intervention decisions by revealing where processes, assumptions, or behaviors are related to unfavorable results.

Predictive Analytics: Anticipating Future Outcomes

Predictive analytics estimates what is likely to happen next by applying statistical and machine learning models to historical and current data. In P&C insurance, predictive models forecast outcomes such as claim frequency and severity, fraud probability, customer churn, litigation risk, or renewal likelihood.

In the rafting analogy, predictive analytics gathers what information is known, such as the geology of the area, prior weather patterns, and current forecasts, to predict the state of the river beyond the upcoming bend.

Predictive outputs — often expressed as scores or probabilities — inform decisions before they are executed. Underwriters use predictive insights to assess risk at quote or renewal. Claims teams use them to anticipate complexity or severity early in the lifecycle. Predictive analytics reduces uncertainty by quantifying future exposure and opportunity.

Prescriptive Analytics: Driving Action and Execution

Prescriptive analytics attempts to determine what should be done. It translates predictive insight into recommended or automated actions, such as routing a claim to a specific handling path, applying pricing adjustments, triggering fraud investigation, or initiating targeted customer outreach.

In the rafting analogy, prescriptive analytics tells you where you might want to position the raft (i.e. in the middle, toward the far bank, etc.) to best handle what may be around the coming bend in the river.

Prescriptive analytics is more than the operational framework for implementing decisions based on information from insurance analytics. As critical as this framework is for achieving value, it can be enhanced with analytics exploring the expected effectiveness or impact of different possible decisions. This is prescriptive analytics.

Prescriptive analytics operates within defined business rules, optimization frameworks, and governance constraints to ensure consistency and control. When embedded into core systems, prescriptive analytics enables real-time execution at scale — turning insight into action without delay.

Why the Closed Loop Matters

Insurers derive the greatest value when all four analytics types operate together. Descriptive and diagnostic analytics provide understanding, but predictive and prescriptive analytics drive outcomes. Without prescriptive execution, insight remains informational. Without feedback into descriptive measurement, decisions cannot be refined.

By aligning descriptive, diagnostic, predictive, and prescriptive analytics within core systems, insurers improve decision accuracy, reduce variability, and capture value from each transaction — strengthening both operational execution and strategic planning.

Top Terms to Know in Insurance Analytics Types

What is it? Analysis that summarizes historical and current insurance data. When is it relevant? During operational monitoring, reporting, and governance activities. What does it do? Establishes visibility into performance metrics and trends. What outcome does it create? A factual baseline for accountability and oversight, and a shared understanding of what has occurred. Examples Dashboards tracking claim frequency and loss ratio trends. What is it? Analysis that explains why observed outcomes occurred. When is it relevant? When performance deviates from expectations or requires intervention. What does it do? Identifies drivers, correlations, and root causes of results. What outcome does it create? Insight into where and why performance issues arise. Examples Analyzing factors contributing to high claim severity in a region. What is it? Statistical and machine learning techniques that use patterns in the data to forecast likely future outcomes. When is it relevant? Before decisions are made, especially when foreknowledge of the outcome would affect the decision made. What does it do? Estimates probabilities and expected values of future events. It informs a decision-maker of what is more or less likely to happen. What outcome does it create? Reduced uncertainty and improved anticipation of risk and opportunity. Examples Predicting claim severity at first notice of loss. What is it? Analytics that recommends or automates actions based on predictions. When is it relevant? At the point of decision execution within insurance workflows. What does it do? Guides or automates optimal actions, reflecting corporate direction based on the predicted information. What outcome does it create? Improved decision execution and measurable performance gains. Examples Routing claims to fast-track or special investigation. What is it? A closed cycle of descriptive, diagnostic, predictive and prescriptive analytics linking insight, decision, action, and outcome. When is it relevant? Across the full insurance analytics lifecycle. What does it do? Ensures decisions are continuously informed and refined. What outcome does it create? Sustained improvement through feedback and recalibration. Examples Using claim outcomes to retrain severity prediction models. What is it? Number of claims divided by earned exposures. When is it relevant? In performance measurement and insurance pricing. What does it do? Indicates the likelihood of a claim happening per exposure. A frequency of 10% indicates that for every unit of exposure, there is a 10% chance that a claim will be filed. What outcome does it create? Visibility into insurance pricing and loss control effectiveness. Examples Measuring the effectiveness of a loss prevention initiative. What is it? Claims paid plus adjustment expenses divided by the number of claims. When is it relevant? In performance measurement and insurance pricing. What does it do? Indicates the cost of insured losses per claim. Does not include expenses not allocated to the specific claim. A severity of $2,500 indicates that the average claim payment for every claim is $2,500. What outcome does it create? Visibility into insurance pricing and loss control effectiveness. Examples Measuring severity trends over time to forecast future costs. What is it? Insured losses divided by earned premium. When is it relevant? In performance measurement. What does it do? Indicates the portion of premium earned that is spent on insured losses. A loss ratio of 65% indicates that 65 cents out of every dollar of premium is used to pay losses. What outcome does it create? Visibility into insurance profitability with respect to losses. Examples Measuring loss ratio across regions to identify unprofitable areas. What is it? A statistical technique that identifies when certain things (e.g. values, outcomes, events) occur together. When is it relevant? During diagnostic, predictive and prescriptive analytics. What does it do? Correlated fields indicate a possible connection. What outcome does it create? Better insights into how certain outcomes occur (diagnostic analytics), which when used within formal modeling frameworks can inform predictions (predictive analytics) and recommendations (prescriptive analytics). Examples A correlation between geographic region and average age indicates that there are patterns on where older and younger people live. What is it? A form of analysis where subsets of the data are looked at to determine differences in their performance from the whole data. This includes subsets of subsets, hence the image of “drilling down” into the data. Drill-down exploration is typically a manual activity. When is it relevant? During descriptive and diagnostic analytics. What does it do? Provides information on the characteristics of smaller parts of the whole data. What outcome does it create? Insight into the characteristics and performance of individual segments of the data. Examples Looking at claim frequency for the company as a whole, and then for a single region, and then for a single class within that region. What is it? A form of analysis where different segments of the data are compared. Comparative analysis is typically a manual activity. When is it relevant? During descriptive and diagnostic analytics. What does it do? Provides information on how different parts of the data compare to each other, or to the whole data. What outcome does it create? Insight into the relative make-up or performance of different parts of the data. Examples Comparing the claim severity across the different regions of a book of business. What is it? Predictive modeling techniques that attempt to relate predictor variables with the target outcome. Statistical models typically have coefficients that are optimized using machine learning techniques, hence the modern interchangeability of the terms. When is it relevant? During predictive and prescriptive analytics. What does it do? Creates predictive models that provide not only predictions but the justifications and proof that they are reliable. What outcome does it create? A predictive model. Examples Linear model, generalized linear model (GLM), generalized additive model (GAM). What is it? Predictive modeling techniques that use machine learning. Machine learning is a form of AI that learns patterns in large datasets. Though the phrase “machine learning models” does include statistical models along with other techniques from the field of computer science, specifying both “statistical and machine learning models” provides clarity on what is being referenced. When is it relevant? During predictive and prescriptive analytics. What does it do? Creates predictive models that provide not only predictions but the justifications and proof that they are reliable. What outcome does it create? A predictive model. Examples Statistical models, tree-based techniques, gradient boosting machines, random forests, neural networks. What is it? A number representing the output of a predictive model. The score is a translation of the prediction into a form that can be more appropriate in some cases. When is it relevant? When the relative prediction is more important than the specific prediction. What does it do? Makes predictive output more useful in some cases. Scores are often more useful for non-technical end users as they automatically provide the context of whether a result is high or low. What outcome does it create? A score that has a range (e.g. 1–10, 1–100, 0–999) indicating higher and lower predictions. Examples Credit score, where having relatively high credit or low credit is more useful for the end user than knowing they have a 15% chance of an insured claim.

Roles and Responsibilities in Insurance Analytics

Insurance analytics is not owned by a single team or function. It is a cross-functional activity that depends on clearly defined ownership, accountability, and collaboration across executive, business, technical, and operational roles. Across the insurance industry, analytics initiatives most often fail not because of insufficient data or models, but because decision rights and responsibilities are unclear across the analytics lifecycle.

The different roles described here do not simply align with the phases of the insurance analytics lifecycle described in the next section. While the importance of the roles does change across the phases, and a simplistic view can line up each phase with a role, well functioning insurance analytics typically involves each role in some way in almost every stage. Analytics translators or “two sport stars” that can bridge communication gaps between teams are especially valuable.

Decisions are made during each stage of the analytics lifecycle. Clarity in the roles and responsibilities involves defining which role has decision authority and which other roles advise and provide important input.

Note that different insurers have different structures with roles of different titles and responsibilities. What is important is that insurers clearly understand who is playing what role. Here we describe common titles and their responsibilities with respect to insurance analytics. Successful insurers organize analytics responsibilities across six core accountability layers:

1. Strategy and Enterprise Accountability

Roles at this layer define why analytics exists and how value is measured.

| Role | Responsibilities |

|---|---|

| Chief Data and Analytics Officers (CDAO) / Chief Data Officers (CDO) | Own enterprise analytics strategy, data and analytics governance, and alignment between analytics investments and business objectives. Establish standards, funding priorities, and accountability for outcomes. |

| Executive and Line-of-Business Leaders | Set risk appetite, profitability targets, and strategic priorities. Use analytics outputs to guide growth, portfolio management, and capital allocation decisions. |

| Enterprise Risk Management | Document and manage the risks associated with the use of AI and predictive models, and reliance on vendors. Conduct audits for period checks that are critical to governance. |

This layer decides what analytics activities are funded, and ensures analytics initiatives are anchored to business outcomes rather than isolated technical success. Roles at this layer benefit from the input and expertise of analytical, IT, and operational experts who can inform them of the consequences of competing options.

2. Data and Technical Architecture

Roles at this layer are responsible for building the data capability.

| Role | Responsibilities |

|---|---|

| Data Engineers and Architects | Design and maintain data structures for quote/bind, policy management, billing, claim adjustment and settlement, data storage, analytics, and external reporting. Design and maintain data pipelines and integration frameworks that allow data to flow between these structures. Ensure data availability, quality, scalability, and performance across internal and external sources. |

| Software Architects | Help select and maintain software used for business intelligence (descriptive and diagnostic analytics) and predictive modeling (predictive and prescriptive analytics). Ensure the security and performance of these tools based on the feedback and requirements of users. |

This layer ensures that data is consistent and available in the right format for various needs, and that tools are available for the extraction, analysis, and reporting of that data.

3. Model Research, Development and Maintenance

Roles at this layer are responsible for building the statistical and machine learning models used in insurance analytics.

| Role | Responsibilities |

|---|---|

| Data Scientists and Actuarial Modelers (Predictive Modelers) | Develop predictive and prescriptive models for underwriting, pricing, claims, fraud detection, and customer analytics. Validate assumptions with domain experts and ensure models are fit for purpose. |

| Business Analysts | Review performance through descriptive and diagnostic analytics. Provide monitoring of operational analytics to ensure consistent performance over time. |

This layer transforms raw data into reliable analytical assets and monitors those assets.

4. Decision Design and Translation

Roles at this layer connect analytics to real-world decisions.

| Role | Responsibilities |

|---|---|

| Domain SMEs and UX | Subject matter experts (SMEs) and user experience professionals (UX) translate analytical insights into decision logic, rules, and workflows that are accessible and understandable for front-line users. Bridge business context and technical outputs. Ensure analytics recommendations align with operational realities, regulatory constraints, and customer expectations. |

| Education and Training Professionals | Develop educational and training materials for users of predictive analytics. Ensure the correct and informed use of the information provided. |

This layer ensures analytics is usable, interpretable, and relevant.

5. Business Operations

Roles at this layer apply analytics at the point of action and are responsible for results.

| Role | Responsibilities |

|---|---|

| Line-of-Business Executives and Operations Leaders | Translate executive priorities to operational initiatives. Execute analytics-driven decisions in real time, requiring engagement with training and the use of new workflows. Collect and pass on feedback from front-line users and domain SMEs on decision effectiveness and usability. |

| Front-line Users and Domain SMEs | Use analytics insights to improve insurer performance. Identify unintended consequences and report on difficulties in using the predictive information and new workflows. Ensure that insurance analytics is not used blindly. |

This layer is where analytics directly influences loss outcomes, expense efficiency, and customer experience.

6. Oversight, Governance, and Feedback

Roles at this layer ensure control, trust, and continuous improvement.

| Role | Responsibilities |

|---|---|

| IT and Core Systems Teams | Support auditability and provenance of data, as well as model deployment, versioning, auditability, and system reliability. Ensure system security for all operational deployments. |

| Risk, Compliance, and Governance Functions | Oversee model validation, fairness, explainability and regulatory compliance. Work with analytics teams to provide proactive advice, internal challenge and review. Work with internal ERM to manage the risks from insurance analytics. |

This layer supports analytics by requiring compliance to standards and managing risk.

When these roles operate in isolation, analytics initiatives stall. When they are aligned to clear decision ownership, insurers achieve higher adoption, faster execution, and stronger return on analytics investment.

Top Terms to Know in Analytics Roles

What is it? Coordinated work across business and technical teams. Cross-functional refers to activity that involves multiple business functions for an insurer, such as executive, underwriting, IT and others. When is it relevant? Throughout the analytics lifecycle. What does it do? Aligns expertise and priorities across business functions. What outcome does it create? Faster delivery and higher adoption. Examples Joint underwriting–data science model reviews. What is it? Not a specific role, but any employee that can bridge the communication and understanding gap between analytics and other business units. Also called a “two sport star” — a sports reference to someone who can play more than one sport at a high level. When is it relevant? Throughout the analytics lifecycle. What does it do? Helps different business units to understand things outside of their expertise. Bridges gaps in communication and understanding. What outcome does it create? Better prioritization, more effective analytics, higher adoption, and reduced misinterpretation. Examples Data scientist who can explain model output in business terms; UX designer who can translate an analytics project into user interfaces. What is it? A generic term for an analytics project that an insurer decides to do. Refers to the entirety of the project, from ideation to model creation, implementation, and monitoring. When is it relevant? During design and deployment of analytics use cases. What does it do? Refers to all the different roles and activities for an analytics project as a whole, single initiative. What outcome does it create? Clarity on the cross-functional nature of analytics projects. Examples An effort to revise the personal auto rating plan; claims triage modeling project. What is it? Clear accountability for a specific insurance decision. Specification of who owns a particular decision, who has the right to make that decision, or who has the authority to make that decision. When is it relevant? At every step of the analytics lifecycle. What does it do? Determines who is responsible for a decision and its outcomes. What outcome does it create? Clarity of roles, consistent execution, and measurable accountability. Examples Predictive modelers choosing which analytics technique to use; executives setting analytics priorities. What is it? The steps involved in an analytics initiative, from start to finish. Refers to a defined process that moves through different stages. When is it relevant? Across the full duration of an analytics initiative. What does it do? Clarifies the full process of an analytics project for everyone involved. Coordinates activities that connect data to decisions and outcomes. What outcome does it create? Consistent, efficient analytics execution. Examples Lifecycle stages from objective definition through feedback integration. What is it? The strategic decision on what kinds of risks to write, and in what amounts. When is it relevant? At underwriting, and in portfolio management and capital allocation. What does it do? Specifies the market that the insurer wants to write and limits exposure to loss by limiting how much is written. What outcome does it create? More consistent and stable results. Examples Limiting the amount of property insurance written in hurricane-prone areas. What is it? The process where insurers specify how much of their capital/surplus is used to support the insurance operations for different lines of business and regions. When is it relevant? Development of business priorities and strategies, corporate goals. Also relevant in portfolio management and regulatory review. What does it do? Specifies the capital required to support operations. What outcome does it create? Trust in the financial stability of the insurer. Context for setting corporate goals and strategy. Examples AM Best review of capital adequacy across an insurer’s lines of business. What is it? Any part of the system architecture which moves data from one function or location to another. Typically involves transforming the data structure to be appropriate for the new use. When is it relevant? Through an insurer’s operations. What does it do? Makes data available for specific uses, translates data from one structure to another. What outcome does it create? Access to required data. Examples Creation of analytics-ready datasets from data storage; use of quote data to generate a predictive output, and application of that output in the quoting system. What is it? The documented history of a data source — where it came from, who was responsible for it, and current data definitions. When is it relevant? Any time data is relied on for a business use case. What does it do? Documents the origin and reliability of data. Maintains trust in analytics inputs. What outcome does it create? Reliable analytics outputs. Examples Record of the data flows which feed a data storage; documentation of vendor-provided data. What is it? Predictive modeling techniques that differ in their origins. Statistical models originate in the field of statistics; machine learning models originate in the field of computer science and are one kind of artificial intelligence (AI). The term “machine learning” is more generic than “statistical” and encompasses modern statistical models along with additional techniques. However, specifying both terms provides additional clarity when predictive modeling is referred to in general. When is it relevant? During predictive and prescriptive analytics. What does it do? Creates predictive models that provide not only predictions but the justifications and proof that they are reliable. What outcome does it create? A predictive model. Examples Statistical models (e.g. GLM, GAM), tree-based techniques, gradient boosting machines, random forests, neural networks. What is it? Generic term for employees with the skills to build predictive models. For insurers, this typically refers to actuaries and data scientists. When is it relevant? During model creation. What does it do? Refers generally to employees building predictive models, whether they are data scientists, actuaries, statisticians, or otherwise. What outcome does it create? Efficient terminology. Examples Actuarial modelers, data scientists.

In Motion: The Analytics Process in Insurance

Insurance analytics operates as a structured, continuous operational lifecycle that connects data, decisions, and outcomes across the property and casualty insurance value chain. This lifecycle is designed to support consistent decision-making, maintain analytical reliability, and adapt to changing data and business conditions over time. Each phase contributes to decision quality, governance alignment, and measurable business impact.

To understand the analytics lifecycle, it is helpful to note that its phases span two different cadences of insurance operations. The first is daily operations, where insurance policies are written and managed, claims are adjusted and paid. This is the speed at which the insurance operations happen. It is the cadence at which new data is generated, and also the cadence at which operational analytics must work in order to inform regular business decisions.

The second cadence is outside of daily operations, when analytics projects are considered, prioritized and planned, and when historical data is aggregated and predictive/prescriptive models are built. This gives insurance analytics a periodic nature, even when the application of insurance analytics is done in real time.

The analytics lifecycle moves through both the periodic, strategic creation of predictive models, and the real time operationalizing of predictive information. The stages enable insurers to move from observation to explanation, anticipation, and execution while maintaining transparency and control. Lifecycle discipline supports repeatability, auditability, and sustained performance as analytics capabilities scale across underwriting, claims, pricing, and customer engagement.

Industry guidance emphasizes the importance of lifecycle management and governance practices to ensure analytical models remain accurate, explainable, and aligned with business objectives throughout their use. Structured oversight supports reliability, regulatory confidence, and long-term value realization in analytics-driven insurance operations.

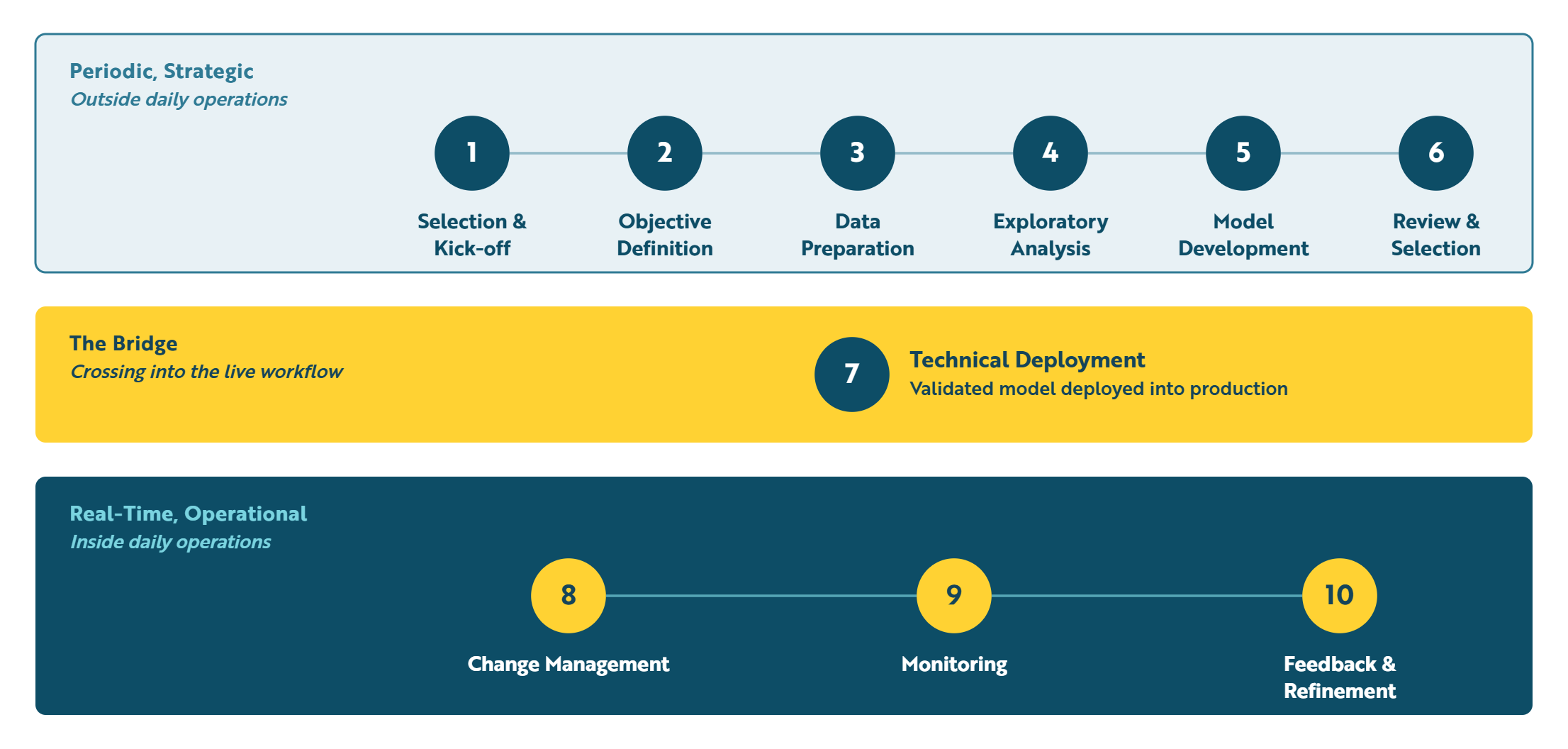

Two Cadences, One Lifecycle

The analytics lifecycle spans two operating tempos. Stages 1–6 happen periodically, outside daily operations. Stages 8–10 run continuously, inside them. Stage 7 is the bridge — the moment a validated model crosses into the live workflow.

Analytics Lifecycle Stages

Note that the Roles discussed in each stage refer directly to the section on Roles and Responsibilities.

1. Selection and Kick-off

Insurance analytics lifecycle begins when an insurer begins a project. However, this necessarily comes after a review of possible projects, prioritization of those projects, and a decision on how to spend resources. The decision to begin an insurance analytics project should align with business goals, and the process should be driven at the executive/business level (see the section on Roles and Responsibilities). This process should also include analytics experts who can advise as to what insurance analytics can and can’t accomplish, as well as the relative efforts involved.

Ideas for possible projects can come from customers or employees, business owners or front-line experts, as well as industry best practices. Descriptive or diagnostic analytics is often used to identify processes or outcomes that could be improved. This stage is not really a part of the lifecycle for any given project, but is a necessary precondition nonetheless.

Decision Roles

- Strategy and Enterprise Accountability

Supporting / Involved Roles

- Business Operations

- Model Research, Development and Maintenance

- Data and Technical Architecture

- Oversight, Governance, and Feedback

2. Objective and Decision Definition

Once a project is kicked-off, the lifecycle begins with clear articulation of the business objective and decision context. This step establishes how analytics will be used, what outcomes are expected, and how success will be measured. Well-defined objectives align analytics initiatives with operational and financial priorities, and clarify what will be needed for implementation, both from a technical side and for change management (i.e. education and training to ensure adoption).

Decision Roles

- Business Operations

Supporting / Involved Roles

- Model Research, Development and Maintenance

- Decision Design and Translation

- Data and Technical Architecture

- Oversight, Governance, and Feedback

3. Data Acquisition and Preparation

Data required to support the defined objective is sourced, integrated, and prepared for analysis. This includes internal insurance data and relevant external data. At this point, the data required is not live, daily-operations data, but rather the stored history of policy transactions and claim payments.

Transactional internal data can be enhanced through two primary means. First, external data from vendors can provide information not collected by the insurer during prior operations. Second, AI techniques based on large language models can turn unstructured insurance data into actionable information for analytics.

Standardization, validation, and governance controls, including verifying and recording the provenance of any data used, ensure data is suitable for analytical use and decision support.

Decision Roles

- Model Research, Development and Maintenance

Supporting / Involved Roles

- Data and Technical Architecture

- Oversight, Governance, and Feedback

- Business Operations

4. Exploratory Analysis and Feature Development

Data is examined to identify patterns, relationships, and variables that influence outcomes. Exploratory analysis informs feature selection and model design by revealing signals relevant to the decision context.

Note that it is important to restrict explanatory data to that which will be known at the time of implementation. For example, a chance of closure model to be generated at the time of quote cannot use any vendor information, such as credit score, that is not ordered until the time of bind.

Decision Roles

- Model Research, Development and Maintenance

Supporting / Involved Roles

- Data and Technical Architecture

- Business Operations

5. Model Development and Validation

Analytical models are developed to estimate outcomes or support decision logic. Statistical and machine learning (AI) techniques are applied in alignment with the defined objective. Collaboration with domain experts ensures analytical outputs reflect operational realities. Models undergo validation to confirm accuracy, robustness, and appropriateness for their intended use.

Decision Roles

- Model Research, Development and Maintenance

Supporting / Involved Roles

- Business Operations

- Oversight, Governance, and Feedback

6. Model Review and Selection

Models developed by the analytical team need to be reviewed and approved by the business owners of the operations to be affected. The expected impact of the model should be discussed, and the possibility of unintended consequences should be considered. The outcome of this review is often more model development and refinements.

When the final model has been selected, the model and all of the material decisions made in its creation should be documented. The review step can also include an internal, but separate, governance committee who reviews the documentation, validation, and appropriateness of the model created.

Decision Roles

- Business Operations

Supporting / Involved Roles

- Oversight, Governance, and Feedback

- Model Research, Development and Maintenance

- Data and Technical Architecture

7. Technical Deployment and Embedded Execution

Validated models are deployed into operational environments where decisions are executed. All of the prior stages in the analytics lifecycle have taken place outside of the scope of daily operations. This phase bridges the gap to daily operations, and subsequent phases are relevant to this real-time cadence as well.

The exact point in the business flow where the modeled information is surfaced should have been decided in phase 1 — Objective and Decision Definition. But this should be reviewed for any changes that have occurred through the process. Decisions about which employees should have access to which pieces of information and at what point in time should be confirmed.

It is also important to determine how the front-line users will interact with the modeled information because decisions made here can impact the technical deployment. For example, the use of large language models as a user interface to the modeled output has different technical requirements than simply exposing modeled output on users’ work screens.

Decision Roles

- Data and Technical Architecture

Supporting / Involved Roles

- Decision Design and Translation

- Business Operations

- Model Research, Development and Maintenance

8. Operational Deployment and Change Management

In order to ensure the new information is used correctly and effectively, the business should implement any education or training required. Employees familiar with the previous workflow will not automatically know what to do when new information is presented or workflows are changed.

Correct information applied incorrectly can not only mute the intended benefit but cause active harm. Again, preparations for this should have been considered in phase 1, but are confirmed and executed during this step.

Decision Roles

- Decision Design and Translation

Supporting / Involved Roles

- Business Operations

- Oversight, Governance, and Feedback

- Model Research, Development and Maintenance

9. Monitoring and Performance Measurement

Deployed analytics are monitored using defined performance indicators. Monitoring provides visibility into predictive accuracy, decision impact, and operational performance as conditions evolve.

Monitoring operates at three levels. At one level it involves the input fields the deployed models rely on in order to detect mix shifts in the data used to create the model. For example, a model created from data with a 90/10 split between renewal and new business may not function correctly if the percentage of new business increases. One advantage of monitoring distributions is that changes can be noticed in real-time through descriptive analytics.

In addition, the prediction of the model should be monitored for accuracy. Depending on the target, this can involve time delays. For example, checking a prediction of a loss metric may require time for losses to be realized and developed.

Finally, the performance metric that should be impacted by the analytics project should be monitored to determine if the new information resulted in changes in performance. For example, did accurate information about claim severity result in better allocation of claims to adjusters resulting in faster claim handling?

Decision Roles

- Business Operations

Supporting / Involved Roles

- Oversight, Governance, and Feedback

- Model Research, Development and Maintenance

10. Feedback and Iterative Refinement

Observed outcomes and performance insights inform updates to objectives, data inputs, or models. When an insurance analytics project becomes operational, it is necessary to monitor the situation and collect feedback. It must be determined that the model appears to be working as intended. Initial feedback from front-line employees using the output of the analytical project can be critical for making necessary adjustments and promoting adoption.

Once adoption has normalized, ongoing feedback and monitoring can point to opportunities for improvement, and also prevents models from becoming stale and ineffective as they age. Operational models will need occasional updates, sometimes as minor refreshes given new data, sometimes as more fundamental rebuilds.

Decision Roles

- Business Operations

Supporting / Involved Roles

- Model Research, Development and Maintenance

- Oversight, Governance, and Feedback

Top Terms to Know in the Analytics Lifecycle