European Insurance Consumer Survey 2026

Table Of Contents

- 1. Introduction

- 2. Customer comfort with AI is levelling overall

- 3. Customers signal they want the right to refer AI decisions to a human

- 4. Consumers do not want insurers to have their data, even if it helps reduce risk

- 5. Anxiety about natural disasters seems to be receding

- 6. Pet owners cautious about AI help

- 7. Cost of living crisis overshadows insurance spending

- 8. Brand is still king but Gen Z turning to AI chatbots for guidance

- 9. Methodology

1. Introduction

The 2026 Guidewire European Insurance Consumer Survey has the latest insights into insurance consumers’ attitudes to insurers and their use of technology.

This year’s report provides the latest soundings of customers on their opinion of insurers, their products, and the use of AI and personal data for services and products.

Additionally and, for the first time, questions about the value of pet insurance products and services have been included. There is evidence of customers’ growing concern about their pet healthcare costs and they are looking for better cover. In this survey we aimed to gather additional insight on this growing trend.

The report has been polling over 4,000 customers annually in the UK, Spain, France and Germany since 2020.

The takeaways

-

AI tolerance is stabilising34% of consumers are comfortable with AI deciding the price of a policy without humans, but 26% say nothing will make them confident in the use of AI in the insurance industry.

-

AI trust hinges on transparency, regulation and a human in the loop39% rank ‘refer to a human’ as the number one confidence builder if they disagree with AI. Transparency follows at 25% with an explanation of why AI made the decision, with an independent regulator also at 25%.

-

Extreme weather is not driving more coverConcern about natural disasters dropped from 43% in 2025 to 39% in 2026. Just 31% have considered climate-risk cover this year, down from 38%.

-

Views on pet insurance vary across EuropeFor those with pet insurance, satisfaction ranges from 76% in France to just 59% in the UK.

-

Cost of living still drives decisions84% of consumers are concerned about the cost of living; 55% are likely to cut insurance spending.

-

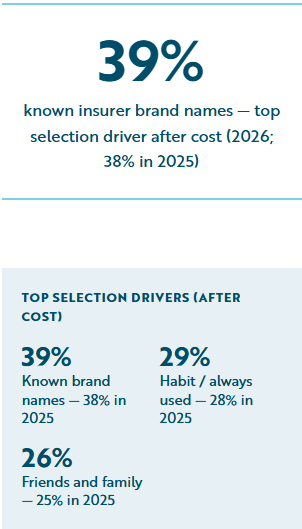

Brand recognition ranks second only to cost39% cite a known brand name as their top driver when choosing an insurer, ahead of habit (29%) and family/friend recommendation (26%).

-

Chatbots and social media are emerging as recommendation tools for younger consumersJust 9% overall, but 21% of Gen Z (18–27 year olds) across the regions surveyed now use chatbots when choosing an insurer.

2. Customer comfort with AI is levelling overall

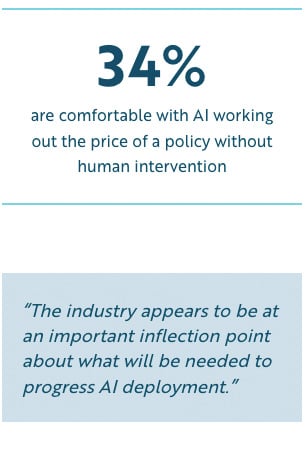

With little overall change in customers’ comfort or discomfort with how insurers use AI, the industry appears to be at an important inflection point about what will be needed to progress AI deployment.

The good news is that more than a third of all customers surveyed (34%) were still comfortable with AI working out price or policy without human intervention, while 26% were neutral about this. The rest (40%) felt uncomfortable, indicating there is still much work to be done on building trust.

Resistance has slightly gone up from 24% in 2025 to 26% in 2026 of respondents saying nothing will make them confident in the use of AI in the insurance industry.

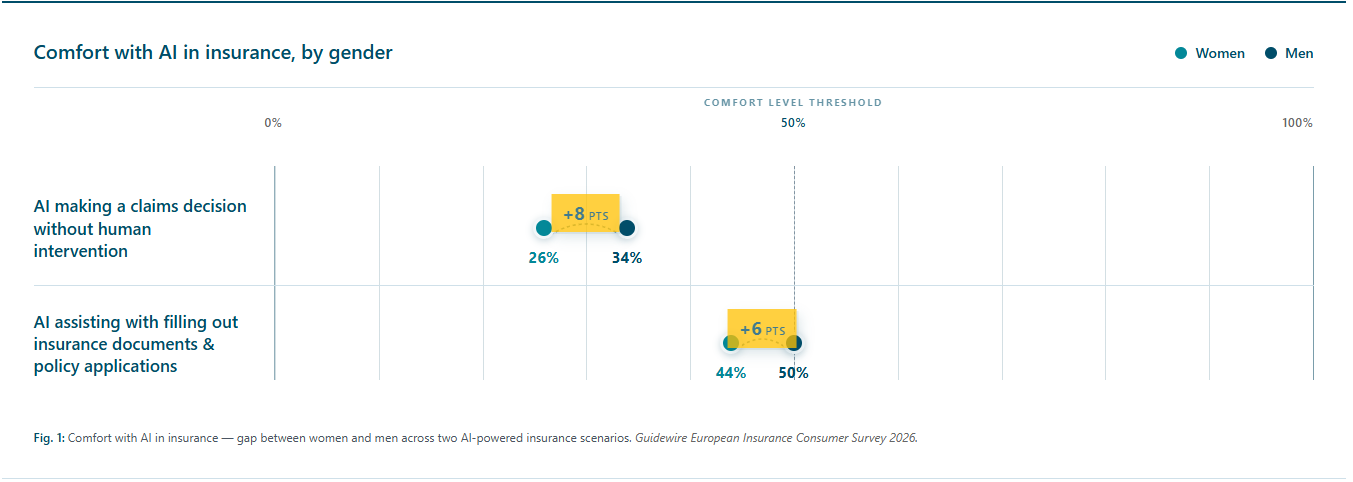

There is a gender divide, too:

- 26% of women respondents were comfortable with AI making a claims decision without human intervention. By comparison, 34% of men were comfortable.

- 44% of women respondents were comfortable with AI assisting them in filling out insurance documents and completing policy applications; 1 in 2 men (50%) were comfortable.

Greater personal use of AI in everyday life is making more customers more amenable to insurers using AI.

Greater personal use of AI in everyday life is making more customers more amenable to insurers using AI. Only 5% of those who use AI tools every day had no confidence in insurers using AI, while 3 in 5 (65%) of those who have never used AI tools had no confidence.

So, it should be positive that the number of customers who said they have never used AI decreased from 28% in 2025 to 21% in 2026. A greater familiarity with AI tools for personal use may be influencing how customers are becoming more receptive to insurer use of AI:

- Close to 1 in 2 of customers aged 18-34 years old (47% 18-24; 48% 25-34 years old) were comfortable with claims processing without human intervention. In 2024 when this question was first asked, the split was 42% of 18-24 and 40% of 25-34 years old. In 2025, the split between the 18-24 and 25-34 age groups was 43% and 48% respectively.

- The +55 age group were not completely against AI usage, especially for self-service; more than 1 in 3 (34%) were comfortable with AI assisting them in filling out insurance documents and completing their policy application.

However, insurers should not just wait for customers’ familiarity with AI to grow and make them more receptive to AI usage because, overall, there is not much movement in customers’ comfort levels year-on-year. The industry needs to continue communicating with consumers and remain transparent with how they use advanced technologies like AI and the direct benefits for customers that these bring.

3. Customers signal they want the right to refer AI decisions to a human

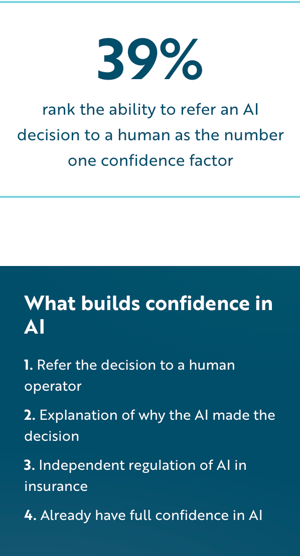

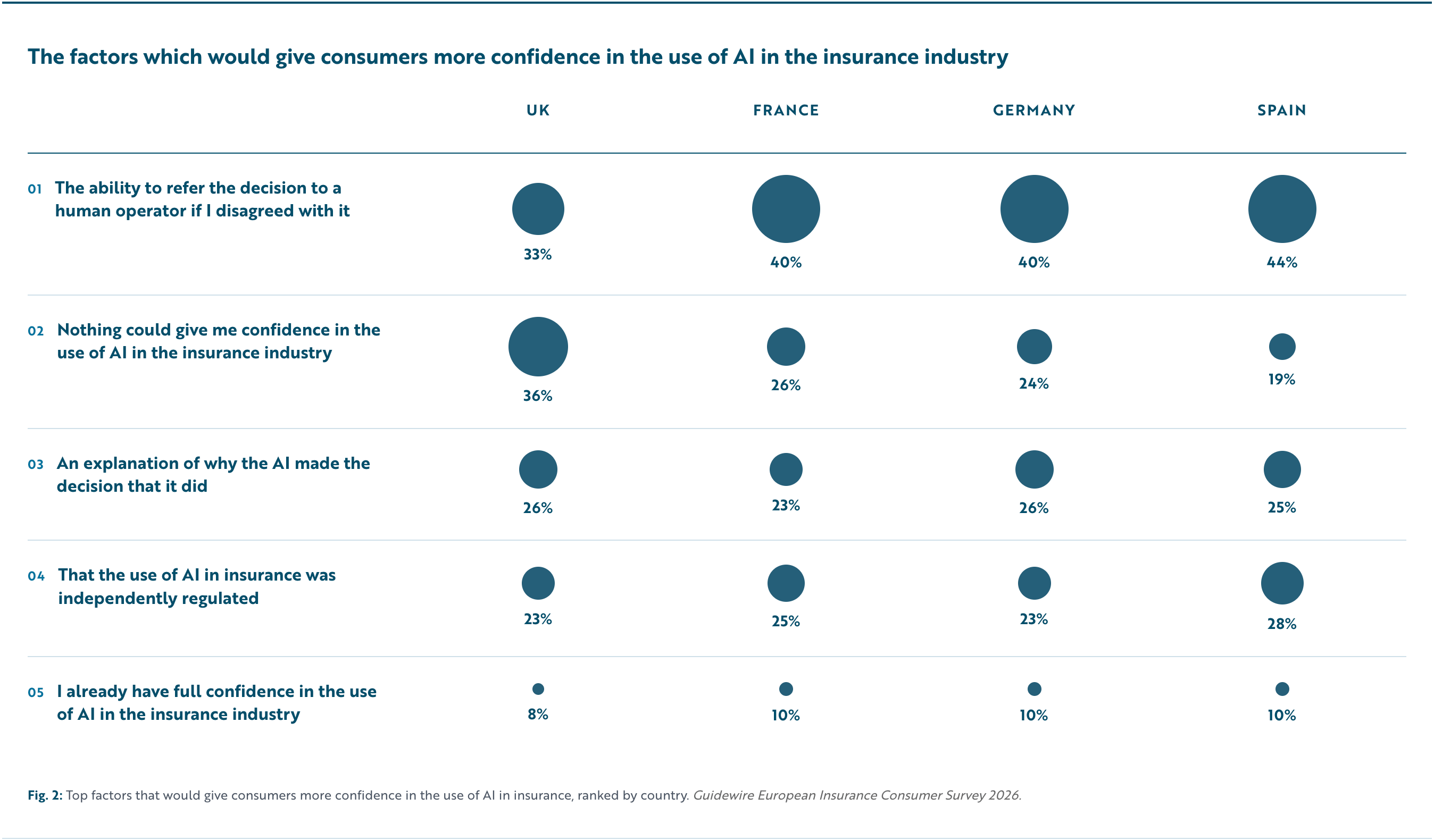

When customers were asked what would give them more confidence in insurers’ use of AI, they ranked as number one the ability to be able to refer to a human if they disagreed with a decision made by AI. This has consistently been the case since 2025 across all markets (39% in 2026; 40% in 2025).

The need for transparency about why AI makes decisions, and an independent regulator, are both moving up slightly to 25% each, respectively, in 2026 (in 2025 the results were 24% and 22%, respectively). Even among those who use AI tools once to a few times a week, the human touch (47%), transparency (30%) and regulation (29%) scored high.

When a customer can see an advantage for them in the insurer using AI, there is greater acceptance:

- When AI is assisting a customer in self-serving a policy application, almost 1 in 2 were comfortable (47%).

- When it is helping an agent to support customers, 41% were comfortable.

On the other hand, customers were uncomfortable with AI deciding and processing their claim, and deciding on the value of the claim without human intervention (47%).

- In the UK and France, customers were split or are cautious about AI helping with documents or supporting call handlers.

- In Germany and Spain, the majority or near-majority were comfortable with AI as an assistant.

Listening to the customers’ need for transparency, regulation, and human oversight, insurers should collaborate among themselves and regulators to better address these concerns.

4. Consumers do not want insurers to have their data, even if it helps reduce risk

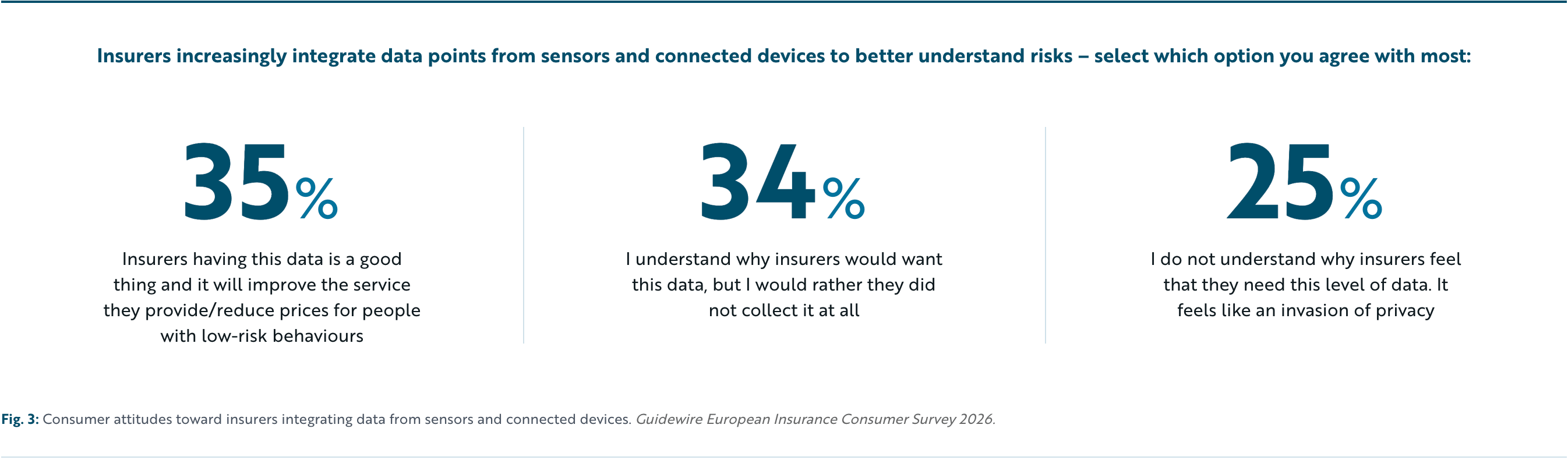

Europeans continue to have mixed feelings about insurers collecting their data from sensors and connected devices.

Over a third of customers either agree or disagree with insurers collecting their data. The number who say they understand why insurers would want this data but would rather they did not collect decreased from 40% in 2024 to 35% in 2025 and now 34% in 2026. This suggests customers are becoming more privacy-conscious and would benefit from more information and assurance about how their data is being safely kept and used.

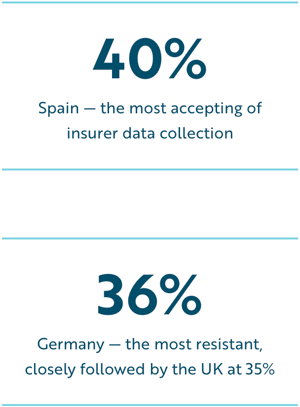

There are national differences in the acceptance of data collection. Spain (40%) was the most accepting of data collection, while Germany showed the most resistance (36%) closely followed by the UK and Spain (both 35%).

In terms of types of data collected, more than a quarter would prefer insurers to collect real-time data about their home’s plumbing (28%) and about their home’s heating (27%).

Other markets seem more open. Spanish customers stand out with higher acceptance of how live data can detect water leakage (36%), followed by French consumers (29%).

These divided views about how the industry uses customer data suggests insurers need to build stronger trust in how they are using personal data and help consumers better understand the value of insurers holding their data. Building trust in how insurers use personal data will play a role in how they generate trust in their use of AI, which depends on access to good data to deliver value to everyone. Acceptance of data collection will rise if customers know that the process is regulated and insurers are complying with relevant safeguards. Indeed, being proactive about how their data collection practices adhere to good governance standards could help insurers positively address this issue.

5. Anxiety about natural disasters seems to be receding

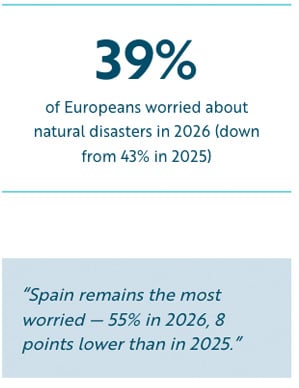

Despite how extreme weather events have affected all markets, customers seem less worried about insuring against damage or loss of property from natural disasters.

Although the concern is dipping in all four markets, there are some differences:

- Spain remains the most worried (55% in 2026, though 8 percentage points lower than in 2025).

- UK customers were the least likely to be worried (21%) and the most likely to not consider the need to purchase natural disaster insurance (66%).

- Germany and France show decreasing willingness to purchase specific insurance to cover damage to your property or your livelihood because of extreme weather risks like flooding or wild fires (58% and 66% respectively in 2026 versus 51% and 56% in 2025).

When insurers offer weather-related insurance policies, customers said they want clearer guidance on what is covered (28% in 2026 and 32% in 2025).

There are some national differences. Germans showed a stronger preference for their insurance provider to offer a risk assessment tool that suggests the right coverage based on their location and property type (27%). French consumers need simple explanations of weather-related insurance terms and how different policies work (27%).

Less concern may reflect a better than expected natural disasters season — but customers may not have enough coverage for potentially very serious damage.

Overall, fewer people considered insurance to cover damage from climate risks (31% in 2026 - 38% in 2025). Spain and Germany continued to be the regions most likely to consider climate risk related insurance (41% and 38% respectively, though these results are 6 percentage points lower than last year's for both).

Less concern about their property being impacted by extreme weather and other natural disasters may reflect a better than expected natural disasters season. However, there are risks that customers may not have enough coverage for potentially very serious damage, given how forecasting natural disasters remains challenging. The potential claims-related fallout when a disaster strikes could leave customers uninsured or underinsured.

6. Pet owners cautious about AI help

For the first time in our annual research, attitudes about pet insurance were surveyed. There are divided views on these products and how technology could help manage the need to visit a vet.

While most countries report high satisfaction rates with 76% of French, 70% of German and 64% of Spanish consumers overall satisfied, the UK does stand out as the least satisfied (59%) with the claims process for pet insurance.

With many pet owners concerned about their pet’s health and keen to know when best to take them to the vet, there could be a market for insurers to provide new services that use AI to offer expert advice and support. The survey finds growing use of online pet health search and symptom checkers among younger age groups with 59% of those aged 18-24 claiming to use them. In Spain, young consumers aged 18-24 were the most likely to use online tools before visiting a vet (76%). The same age group in Germany, UK and France (59%, 46% and 56% respectively) said they also check digital channels. These findings support the case for guided, responsible digital triage that pet insurers could support and enhance.

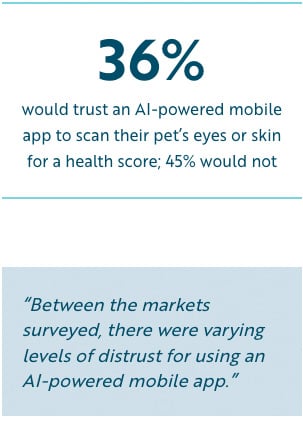

The survey also examined whether consumers would trust an AI-powered mobile app that scans their pet’s eyes or skin to provide an instant health score. More than a third (36%) said ‘yes’, while 45% said they would not trust it.

Between the markets surveyed, there were varying levels of distrust for using an AI-powered mobile app. For example, 1 in 2 French (52%) and UK (50%) customers did not trust an app of this kind. Spain stands out with a higher percentage of customers saying they would trust such an app (43%) versus not trusting it (35%). Also, while more German customers said they distrusted the app (42%), the margin over those who would trust it was slender at 1 percentage point (41%).

Pet owners love their insurer. They are still cautious about an algorithm helping out.

There is room for insurers to change these attitudes about digital tools to be used by pet owners to manage their pets’ health requirements. For example, the proportion of customers who were unsure about an AI-powered mobile app that scanned their pet’s eyes or skin to provide an instant health score or risk triage was almost 1 in 5 customers (19%) across all markets.

It is also worth noting that despite some reported high satisfaction rates with pet insurance there is scope for improvement that can be achieved through new products and services that better recognise how customers' attitudes to their pets is much more complex and sensitive than how they regard insurance cover for their property and possessions.

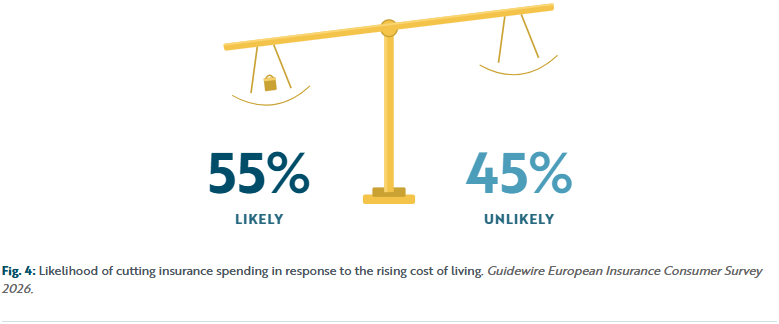

7. Cost of living crisis overshadows insurance spending

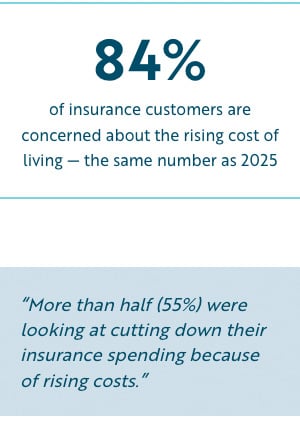

Insurance customers continue to be anxious about the rising cost of living, with 84% (the same number as 2025) saying that they were worried. More than half (55%) were likely to cut down their insurance spend because of rising costs, but much less than half (40%, the same number as in 2025) were likely to cancel an insurance policy completely.

Spanish customers were the most likely to cut down on their insurance spending (63%), closely followed by the French (62%). British customers, on the other hand, were the least likely to do so (44%).

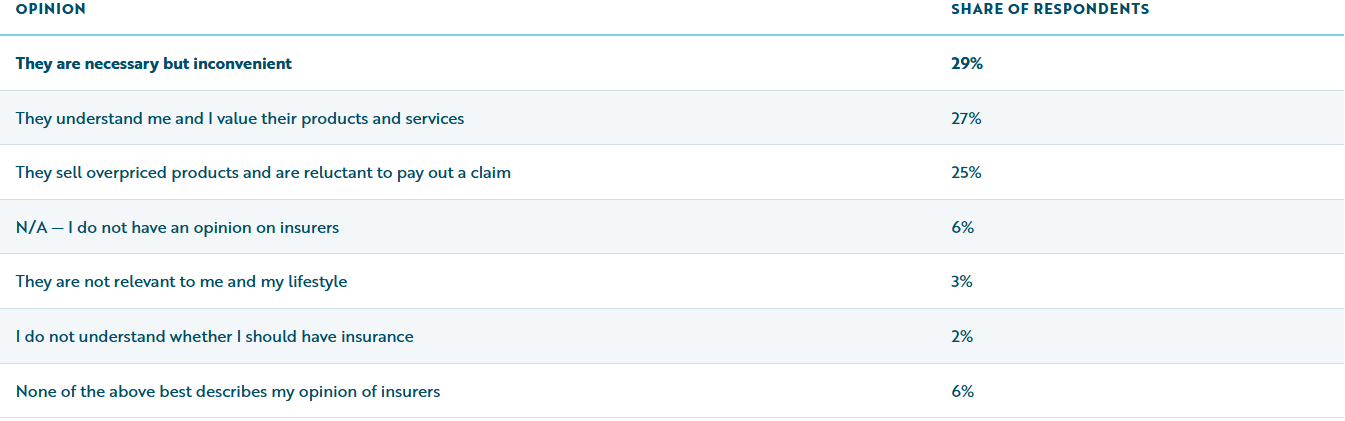

Perceptions of insurers’ value and behaviour have remained stable, with 29% viewing insurers as necessary but inconvenient (30% 2025). Overall, fewer people felt understood by insurers compared to the previous year (27% in 2026 and 32% in 2025). There has also been some criticism that products are overpriced, especially by French and Spanish consumers (32% and 26% respectively).

The efforts made by insurers to improve communication and engagement with customers always benefit from ongoing review and reassessment. One new finding of this survey is that, despite insurers being required in some markets like the UK to be more transparent about price rises, almost half of the customers (43%) surveyed still felt that such premium increases were not clearly communicated. This sentiment was felt despite insurers complying with rules on explaining increases in their customer communications.

Cost-cutting intent

With the significant increase in the cost of living, how likely or unlikely is it that you would cut your spending on insurance?

This attitude is mutual across most markets with the UK (45%), Spain (45%) and France (47%) agreeing that their insurer has not provided them with a clear and transparent explanation as to why their premium increased at the time of renewal. Germany is the only country that thinks otherwise, as almost half of the consumers (49%) said that they believed they had received a clear explanation.

An insurance model that can help customers manage costs is usage-based insurance (UBI), but interest in these products seems to have dipped. The survey found usage of UBI products has gone back to 2024 levels, with 25% of Europeans confirming they have one compared to 24% in 2024 and 29% in 2025. In the UK, customers with a UBI policy fell back to 15% in 2026, 5 percentage points less than last year. There is a similar pattern in Germany (30%) and Spain (25%), both of which have decreased by 4 and 7 percentage points since 2025.

Which of the following best describes your opinion of insurers, if any?

8. Brand is still king but Gen Z turning to AI chatbots for guidance

Customers revealed their key factors for choosing their insurer while providing further insights on how embedded finance is evolving.

Looking at embedded insurance and how much customers would be comfortable choosing insurance products from non-insurers but well-known consumer brands, acceptance remains stable:

- Almost half (47%) said they are comfortable with buying an insurance product alongside the purchase of goods from manufacturers, including IKEA, Amazon or Tesla — a figure that remains similar to last year’s 48%, and 44% and 45% in 2023 and 2024, respectively.

- Although Spain’s comfort levels have dropped from 66% in 2025 to 56% in 2026, the country’s insurance consumers are still the most accepting.

- Similarly, in the UK, acceptance remains somewhat stable from 45% last year to 42% in 2026.

The use of AI chatbots and social media for choosing insurers and products remains nascent overall (9%), but the report suggests that they are becoming more meaningful among younger consumers.

- In the UK, Gen Zs (18-24) used chatbots and social media communities - 23% and 20% respectively.

- Similarly, in Spain, 25% of Gen Zs used chatbots and 23% social media communities.

- In Germany, 27% of consumers in the same age group used chatbots with 17% using social media.

- In France, 25% of Gen Zs used chatbots with 20% using social media.

9. Methodology

The research was conducted by Censuswide with 4,004 Consumers who have bought or renewed a general insurance product or made a claim under it in the last 12 months across the UK, France, Germany and Spain between 13.01.2026 - 22.01.2026. Censuswide is a member of the Market Research Society (MRS) and the British Polling Council (BPC), and a signatory of the Global Data Quality Pledge. We adhere to the MRS Code of Conduct and ESOMAR principles").

Liked this report?

Discover how Guidewire helps insurers across Europe build trust, modernise operations, and deliver products that meet customers where they are. Stay informed with the latest industry research, product updates, and customer stories.

Learn More